Sales of new single-family homes posted the first annual gain in

seven years as median prices continued to rise. The median price of new

homes increased to $248,900 last month, a 1.34% increase compared to

November. The median price of new homes sold was up 13.86% compared to a

year ago.

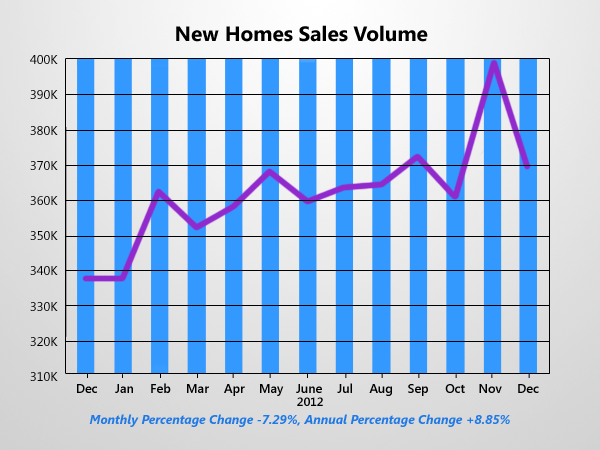

New home sales volume increased nearly 20% from 2011 to 2012, and although the gains were large, sales last year were still the third worst on record. For all of last year 369,000 new homes were sold – about a third of the record number of sales reached in 2005. In December alone – the latest month available – new home sales dropped 7.29% compared to the previous month.

Existing home sales tell a similar story with volume easing December

but remaining well above a year ago. Meanwhile, very limited inventory

maintained the upward momentum in home prices. Total existing home sales

declined 1.00% to a seasonally adjusted annual rate of 4.94 million in

December from 4.99 million in November.

Despite the minor down-tick in December, annual volume was still 12.76% above the 4.38 million-unit level attained in 2011. It was the highest volume since 2007 when it reached 5.03 million and the strongest increase since 2004.

The national median existing home price for all housing types was $180,800 in December, which is 10.97% above December 2011. This is the 10th consecutive month of year-over-year price gains and was the strongest annual price gain since 2005 when the median price rose 12.40%.

New home sales volume increased nearly 20% from 2011 to 2012, and although the gains were large, sales last year were still the third worst on record. For all of last year 369,000 new homes were sold – about a third of the record number of sales reached in 2005. In December alone – the latest month available – new home sales dropped 7.29% compared to the previous month.

Sales Volume & Median Prices

Despite the minor down-tick in December, annual volume was still 12.76% above the 4.38 million-unit level attained in 2011. It was the highest volume since 2007 when it reached 5.03 million and the strongest increase since 2004.

The national median existing home price for all housing types was $180,800 in December, which is 10.97% above December 2011. This is the 10th consecutive month of year-over-year price gains and was the strongest annual price gain since 2005 when the median price rose 12.40%.

Housing is on the march once again, particularly in new construction

starts which saw a strong upsurge in housing starts in December.

Specifically, new construction jumped to a seasonally adjusted annual

rate of 954,000 units. That was 12.1% above the November estimate of

851,000 home starts. In addition, the most recent figure was 36.87%

higher than the December 2011 level of 697,000 homes.

For comparison purposes, though, the figure was still more than 30%

below the average level of housing starts over the past 50 years. Thus,

while housing is definitely on the mend, it still has further to go. For

the most recent year, as a whole, an estimated 780,000 housing units

were started. That was up 28% from the comparable 2011 full-year

estimate, keeping in mind that about 1.5 million starts annually are

needed to keep up with population growth.

For comparison purposes, though, the figure was still more than 30%

below the average level of housing starts over the past 50 years. Thus,

while housing is definitely on the mend, it still has further to go. For

the most recent year, as a whole, an estimated 780,000 housing units

were started. That was up 28% from the comparable 2011 full-year

estimate, keeping in mind that about 1.5 million starts annually are

needed to keep up with population growth.

In addition to new starts, privately owned housing units authorized by building permits came in at a seasonally adjusted annual rate of 903,000 homes in December. That metric, too, was up, albeit nominally, from the estimated 900,000 permits issued in November. The year-to-year swing however was dramatic, with a 28.82% increase in building permits overall for 2012.

Housing completions, which have vacillated up and down consistently throughout 2013, also finished the year strong reporting a 13.20% increase at 686,000 completed units, up from 675,000 in December 2011.

Meanwhile, in a rare bit of uniformity, starts were up in every region of the country in December. Specifically, building was higher by 21.4% in the Northeast, where building had earlier been limited by the ravages of Hurricane Sandy. Moreover, starts jumped by 24.7% in the Midwest, by 3.8% in the South, and by 18.7% in the West.

Taken as a whole, there was little not to like in this report, which was materially better than forecast, and should set this sector up for a stellar 2013. The housing data may not be a game changer at this point, but the December increase in building gives us some confidence that the nation’s gross domestic product will in fact rebound higher in 2013.

In addition to new starts, privately owned housing units authorized by building permits came in at a seasonally adjusted annual rate of 903,000 homes in December. That metric, too, was up, albeit nominally, from the estimated 900,000 permits issued in November. The year-to-year swing however was dramatic, with a 28.82% increase in building permits overall for 2012.

Housing completions, which have vacillated up and down consistently throughout 2013, also finished the year strong reporting a 13.20% increase at 686,000 completed units, up from 675,000 in December 2011.

Meanwhile, in a rare bit of uniformity, starts were up in every region of the country in December. Specifically, building was higher by 21.4% in the Northeast, where building had earlier been limited by the ravages of Hurricane Sandy. Moreover, starts jumped by 24.7% in the Midwest, by 3.8% in the South, and by 18.7% in the West.

Taken as a whole, there was little not to like in this report, which was materially better than forecast, and should set this sector up for a stellar 2013. The housing data may not be a game changer at this point, but the December increase in building gives us some confidence that the nation’s gross domestic product will in fact rebound higher in 2013.

Springtime belongs to the real estate market. It is the season that

brings out the best in buyers looking for a new home. Market activity

will be high and new home sales will soar. With all this going on, when

should serious home sellers list their homes? The answer: right now.

With continued historically low interest rates, buyers have jumped

off the fence and began to seek out available properties for sale. That

is why the smartest move you can make is to list your home as soon as

possible.

With continued historically low interest rates, buyers have jumped

off the fence and began to seek out available properties for sale. That

is why the smartest move you can make is to list your home as soon as

possible.

Since housing inventory is low during the winter months, homes that are listed now have less competition. Your home can be a stand-out instead of being buried under the influx of inventory will come later in March and April. Take advantage of this crucial exposure because when summer hits, the volume of homes for sale will skyrocket.

This year is going to be one of the strongest years in recent memory for buying real estate. When a slumping housing inventory is coupled with high buyer demand, home prices are bound to rise. Since buyers wants to pay the best price possible, they will be motivated to buy now – before prices go up.

Rising home prices can also means a corresponding increase in interest rates. Today’s buyers have the lowest interest rates available in decades which give them the power to buy “more home” without an increase in their monthly housing payment.

If a buyer purchased a $200K home with a 4.65% interest rate, their mortgage payment would be around $1013 per month. Now with rates as low as 3.65%, they would be able to buy a home worth $225K, with no increase in their monthly payment. This gives buyers an extra $25,000 of buying power without increasing the monthly cost of their home.

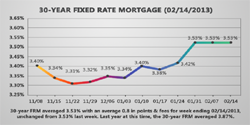

With the Federal Reserve’s quantitative easing policy put in place September of 2012, home lending rates dropped again to historically low levels. At the current rate of 3.32%, home buyers are shopping aggressively before this QE3 policy comes to an end.

Recently several Federal Reserve board chairmen raised concerns regarding the financial stability of this economy as a result of this plan of pouring over $40 billion dollars a month. With these concerns in the air and the possibility that this most recent stimulus may come to a halt, it can be expected that interest rates will increase affecting the requisite buying power of those seeking to purchase a home.

A record number of homeowners, having lost their home due to foreclosure, are now choosing to rent instead of buy property. The high demand for rentals, and a general lack of supply, has actually increased rental rates beyond a typical monthly mortgage payment would be. With the market dynamic being that it is cheaper to buy than to rent, you have yet another solid reason to list your property for sale. If ever there was even a time to put a home on the market, it is right now.

This unique combination of market conditions, including extremely low interest rates, buyers in the marketplace with more buying power, low housing inventory and mortgage payments being cheaper than rent, should be the greatest motivators for you, the home seller, to list your home sooner rather than later. If you take advantage of today’s market conditions you will sell your home in no time at all.

Since housing inventory is low during the winter months, homes that are listed now have less competition. Your home can be a stand-out instead of being buried under the influx of inventory will come later in March and April. Take advantage of this crucial exposure because when summer hits, the volume of homes for sale will skyrocket.

This year is going to be one of the strongest years in recent memory for buying real estate. When a slumping housing inventory is coupled with high buyer demand, home prices are bound to rise. Since buyers wants to pay the best price possible, they will be motivated to buy now – before prices go up.

Rising home prices can also means a corresponding increase in interest rates. Today’s buyers have the lowest interest rates available in decades which give them the power to buy “more home” without an increase in their monthly housing payment.

If a buyer purchased a $200K home with a 4.65% interest rate, their mortgage payment would be around $1013 per month. Now with rates as low as 3.65%, they would be able to buy a home worth $225K, with no increase in their monthly payment. This gives buyers an extra $25,000 of buying power without increasing the monthly cost of their home.

With the Federal Reserve’s quantitative easing policy put in place September of 2012, home lending rates dropped again to historically low levels. At the current rate of 3.32%, home buyers are shopping aggressively before this QE3 policy comes to an end.

Recently several Federal Reserve board chairmen raised concerns regarding the financial stability of this economy as a result of this plan of pouring over $40 billion dollars a month. With these concerns in the air and the possibility that this most recent stimulus may come to a halt, it can be expected that interest rates will increase affecting the requisite buying power of those seeking to purchase a home.

A record number of homeowners, having lost their home due to foreclosure, are now choosing to rent instead of buy property. The high demand for rentals, and a general lack of supply, has actually increased rental rates beyond a typical monthly mortgage payment would be. With the market dynamic being that it is cheaper to buy than to rent, you have yet another solid reason to list your property for sale. If ever there was even a time to put a home on the market, it is right now.

This unique combination of market conditions, including extremely low interest rates, buyers in the marketplace with more buying power, low housing inventory and mortgage payments being cheaper than rent, should be the greatest motivators for you, the home seller, to list your home sooner rather than later. If you take advantage of today’s market conditions you will sell your home in no time at all.

-

Mortgage News

Fixed mortgage rates remained unchanged from the previous week and maintaining near record lows as they continue to support housing demand, translating into a pick-up in home prices in most markets. Meanwhile, homeowners are waiting for Congress to pass a law to make it easier to refinance mortgages with the hope that low rates will [...]

Fixed mortgage rates remained unchanged from the previous week and maintaining near record lows as they continue to support housing demand, translating into a pick-up in home prices in most markets. Meanwhile, homeowners are waiting for Congress to pass a law to make it easier to refinance mortgages with the hope that low rates will [...]

Insider Quotes

“Although affordability in 2012 was highest on record, the excessively tight underwriting precluded many would-be homebuyers from locking-in generational low interest rates. Rising home prices and a gradual uptrend in mortgage interest rates will offset improvements in family income, still 2013 likely will be the third best on record in terms of household buying power. [...]

“Although affordability in 2012 was highest on record, the excessively tight underwriting precluded many would-be homebuyers from locking-in generational low interest rates. Rising home prices and a gradual uptrend in mortgage interest rates will offset improvements in family income, still 2013 likely will be the third best on record in terms of household buying power. [...]

Buyer Tips

Before you let yourself fall in love with that longed-for perfect home and make an offer, you need to seriously seek answers to the questions below so you will know how to confidently invest your money without any surprises or regrets. Understanding property values, home sellers, possible property shortcomings, and the workings of distressed sales [...]

Before you let yourself fall in love with that longed-for perfect home and make an offer, you need to seriously seek answers to the questions below so you will know how to confidently invest your money without any surprises or regrets. Understanding property values, home sellers, possible property shortcomings, and the workings of distressed sales [...]

Seller Tips

Home maintenance takes dedication plus an investment of time and money. Keeping your home in top shape pays off in the long-term by preventing costly replacements caused by neglect or undetected problems. The cost associated with your home maintained and in good repair are fractional when compared to the full replacement cost of systems like [...]

Home maintenance takes dedication plus an investment of time and money. Keeping your home in top shape pays off in the long-term by preventing costly replacements caused by neglect or undetected problems. The cost associated with your home maintained and in good repair are fractional when compared to the full replacement cost of systems like [...]

Useful Links

To help analyse and understand the plethora of data that is available, the National Association of Realtors produces a series of Local Market Reports (LMRs) to provide insight into the fundamentals and direction of the nation’s largest metropolitan housing markets. To find a local market report in your area please visit the National Association Of [...]

To help analyse and understand the plethora of data that is available, the National Association of Realtors produces a series of Local Market Reports (LMRs) to provide insight into the fundamentals and direction of the nation’s largest metropolitan housing markets. To find a local market report in your area please visit the National Association Of [...]